Soaring aerospace parts: General Industry Coverage

With a global commercial aircraft order backlog recently valued at $920 billion, jetliner and jet-engine builders are placing volumes of part orders not seen for many years -- if ever.

To understand just how healthy the market for new commercial jetliners is, pay a visit to the desert where the old ones go to die. Over the past 5 years, U.S. airlines have retired nearly 1,300 planes, or 21.7 per month, to various desert storage areas, according to an Associated Press report. In the past, these planes might have been lined up neatly in rows, sealed and returned to service when airline traffic increased. Now, many of them are going straight to the desert scrap heap in favor of new, more fuel-efficient jets.

Indeed, airlines around the world are on the biggest-ever binge of commercial jet buying, ordering more than 8,200 new planes over the past 5 years from Airbus and Boeing alone, according to AP.

“The most important theme in aerospace is the unprecedented growth spurt in the civil aviation market,” said Richard Aboulafia, vice president of analysis for Teal Group Inc., an aerospace and defense consulting firm based in Fairfax, Va., during a presentation at the AMT Global Forecasting & Marketing Conference, held Oct. 14-16 in Cincinnati. “It’s astonishing, and while I am concerned that a lot people are banking on these growth rates continuing and would advocate a more conservative approach going forward, it’s been a great ride. This is a big business at its peak.”

Parts Bonanza

With record-setting order backlogs, jetliner and jet-engine builders are placing volumes of part orders not seen for many years—if ever. “It’s a giant tsunami just brewing,” said Kevin Flanagan, director of sales and marketing for Glastonbury, Conn.-based Flanagan Industries LP, a jet-engine parts maker, in an article by the Hartford Courant.

Business information provider Bloomberg LP, New York, reported that in September the global commercial aircraft order backlog was valued at $920 billion. Jet-engine builder Pratt & Whitney, East Hartford, Conn., expects to double engine production from current levels by the end of the decade.

Another aerospace parts manufacturer, Pegasus Manufacturing Inc., Middletown, Conn., will be adding a shift to meet demand for aerospace parts, according to the Hartford Courant. The company expects to double its revenue by 2018 and more than double its staff, from 75 to about 175. The shop also expects to log 340,000 man-hours when production peaks in 2018. In 2013, Pegasus logged 90,000 man-hours.

Civil Sensation

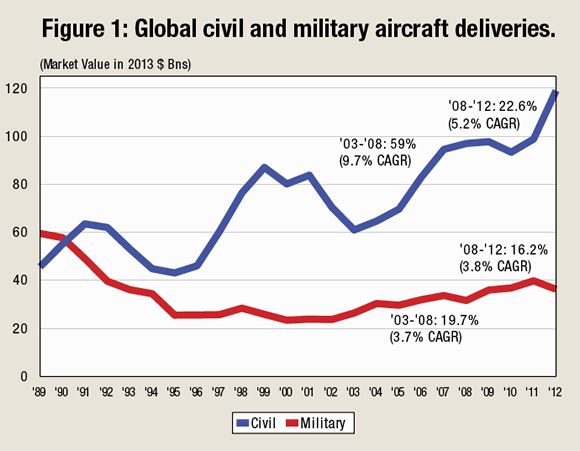

A huge portion of the parts made by aerospace suppliers are going into civil aircraft, which have grown to dominate the aerospace industry compared to military aircraft (Figure 1). For example, in 2012, the market value of global civil aircraft deliveries reached $118.9 billion, compared to just under $36.7 billion for military aircraft deliveries, according to Teal Group. Compare that to 1989, when the military aircraft segment was top dog, at about $60 billion, while civil aircraft deliveries brought in under $50 billion (all figures are calculated in 2013 dollars and based on actual, not list, prices).

At $88.1 billion, large jetliners accounted for the vast majority of 2012 civil deliveries, more than doubling its total of $40 billion in 2003. What’s more, the large jetliner market continued to grow through the Great Recession.

Courtesy of Teal Group

“As we all know, in 2009 the global economy declined, and that should have precipitated something bad in the jetliner [building] market,” Aboulafia said. “But, like the proverbial Energizer Bunny, it just kept going.”

From 2008 to 2012, which includes the Great Recession and the sluggish economic recovery that followed, large jetliner deliveries shot up 57.4 percent, even while business aircraft deliveries dropped 29.2 percent, regional jets fell 29.2 percent and civil rotorcraft dipped 15.2, according to Teal Group (Figure 2).

‘Rip in the Fabric’

“What is different is that there has been a blatant rip in the fabric of the jetliner universe,” Aboulafia said. “We’ve never seen this massive bifurcation between the cost of fuel and the cost of cash, which used to rise and fall in tandem. Look at it from the airlines’ perspective. Interest rates for loans to buy jets are very low. In the past, when oil was $25 a barrel, why [should the airlines] bother replacing jets? Their fully depreciated DC-9s were looking great, the passengers weren’t complaining, so why not keep them in service?”

However, today’s oil prices are nearly four times that figure, at $95 per barrel. In times past, when fuel was expensive, interest rates on loans were expensive too, and airlines typically could not afford to pay for a retooled fleet. “But over the past 5 years, for the first time ever, when airlines really wanted to replace old, fuel-guzzling jets because oil was over $100 a barrel, they could get low-interest loans,” Aboulafia said. “And there’s also a third factor here: From a third-party capital provider standpoint, [when these loans were being made] there really weren’t many other games in town [where capital could go]: emerging markets, real estate, technology stocks—no one wanted them.” Historically, large jetliner financing and leasing has been a stable, reliable market, so the money poured in.

Review the print ads from this magazine to continue

This quick advertiser review unlocks the rest of the article and keeps the full-screen reader focused on the ads instead of the page chrome.

MFGAxis Discussion