The future’s so bright…

The U.S. manufacturing industry continues to make gains in most sectors.

Significant growth is occurring in practically every U.S. manufacturing sector, including automotive, electronics and general industry, according to Gustavo Sepulveda, robotics and business automation head at Panasonic Connect North America in Hoffman Estates, Illinois. “I have not seen, in the last 25 years, a better moment to be in manufacturing.”

One prominent reason is more nearshoring, he added, as U.S. companies want manufacturing to take place as close as economically possible to minimize any future potential risk, such as another pandemic or logistic snags that cause a lack of components. Sepulveda’s area of expertise is helping to overcome the latter now and in the longer term. “Because companies need to grow, and due to the lack of personnel, they are automating more and more.”

The automation initiatives involve equipment and programming purchases, Sepulveda said. “I see a very strong marriage between hardware and software, and you do not see anyone buying hardware without buying software and vice versa.”

As manufacturers grow along with their automation footprints, Sepulveda emphasized that robots and other labor-saving automation equipment is not enough to maintain that development — more human workers are required.

“There is the myth that automation eliminates jobs. It is exactly the opposite,” he said, adding that automation also improves worker safety and part quality, and generates more revenue. “If you see the countries in the world with the lowest unemployment rates, what a coincidence that those countries have the highest density of robots.”

Machine Movement

One sector that is experiencing slower output and a decline in new orders this year compared to 2022 is machine tools, said Director of U.S. Industries Mark Killion, a chartered

financial analyst at Oxford Economics USA Inc. in Wayne, Pennsylvania. But that situation is not necessarily negative because machine tool builders were trying to catch up in the previous year as customers placed a lot of new orders to deal with their own issues, such as supply chain snarls.

“It has been a transition year this year for the machine tool industry,” Killion said. “This year things have calmed down a bit. It’s allowed the industry to stabilize inventory levels a bit and to have the high backlog of orders that were in place previously to be worked off.”

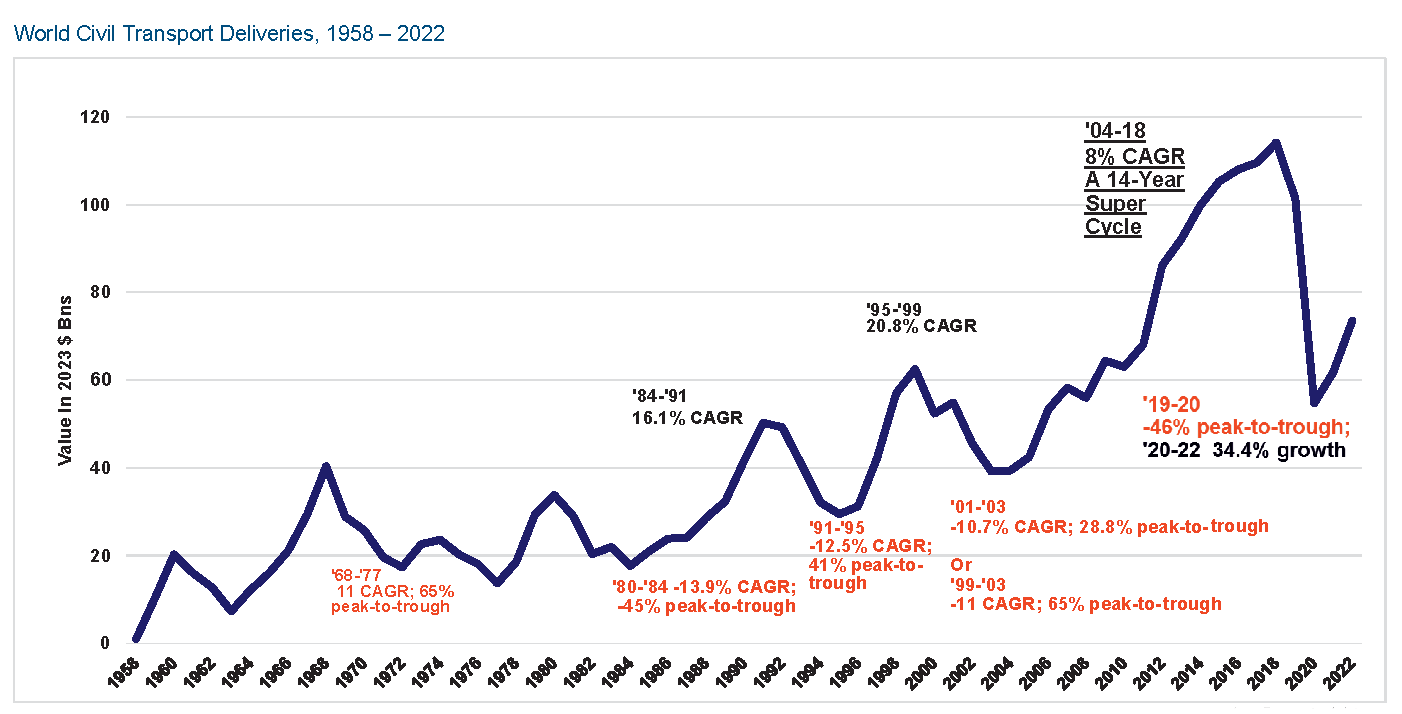

World civil transportation delivery from 1958 to 2022 shows a recent savage drop followed by a tepid recovery in the jetliner business cycle. Image courtesy of AeroDynamic Advisory

One trend, he noted, is that the average cost of a machine tool has increased during the past few years, which reflects the extra value-added features many machines offer to help overcome ongoing labor challenges.

“It is one of the reasons why there is a greater demand on the part of many customers for productivity-enhancing features, such as software and connectivity,” Killion said. “Trying to keep up the output with the same amount or even a smaller amount of workers is something that a lot of manufacturers are facing — not by choice but out of necessity.”

In addition to enhancing machinery, manufacturers are upgrading the skills of their workforces — upskilling, Sepulveda said. For example, workers who were just moving workpieces from one cell to another are now being trained to program robots that will move the pieces instead. “A lot of our customers are asking us to have a permanent trainer because they want to upskill all their personnel.”

Up in the Air

The aerospace environment is also changing as the industry’s supply chain faces numerous bottlenecks, with labor on top, according to Richard Aboulafia, managing director of AeroDynamic Advisory LLC headquartered in Ann Arbor, Michigan. Other shortages include microchips, forgings, chemicals and resins, castings, machined parts, and supplies of superalloys and titanium mill product and sponge.

“This is the first time in my 35 years where the demand side doesn’t matter very much,” he said. “It’s supply-side challenges. Thought I’d never see that. I look at markets, markets and markets, and all of a sudden for the first time it’s really the production side that is having issues.”

Compounding the worker shortage for commercial aviation is that the defense side is competing for the same technical skills and their bait is generally more enticing, Aboulafia said. “With defense being as high as it is, and defense spending usually more of a cost-plus business where you don’t have to worry about how much you pay them, getting talent in the commercial side just is an ongoing challenge.”

Another concern is the new generation of single-aisle engines. “There are only two new-generation single-aisle engines,” he said. “Both have had problems, a bunch of problems.”

The latest one was the recall by Airbus supplier RTX of 1,200 Geared Turbofan engines built by its Pratt & Whitney subsidiary, which was prompted by microscopic contamination in the powdered metal used to make high-pressure turbine discs for engines, leading to a risk of microcrack accumulation.

A Panasonic modular chip mounter in use at Lorain Country Community College. Image courtesy of Panasonic Connect North America

Aboulafia noted that the new-generation engines require more maintenance because of the engines’ higher performance levels, higher operating temperatures and higher pressures. “A lot of them were sold with guaranteed cost agreements, sort of power-by-the-hour type contracts, so there could be a hit to engine makers’ profitability in some cases.”

Nonetheless, with supply side challenges for the industry, older engines and other equipment needs to remain in service longer, he said. “It’s a growing concern because it’s pretty labor-intensive and labor is the heart of the problem here. On top of that, you had an awful lot of people deferring maintenance during the pandemic, nonessential maintenance, so that is all coming due. It’s creating a bit of an MRO super cycle — a huge challenge.”

One big trend that continues is the shift from twin- to single-aisle airplanes, Aboulafia noted, as the backlog and deliveries by value for both Airbus and Boeing twin-aisle offerings were at their lowest levels in 2022. Single-aisle planes can travel increasingly longer distances, “doing routinely 3,000 to 4,000 nautical mile routes. The real power of this is when the A321XLR version shows up in about a year or so. That’ll do north of 4,000 nautical miles.”

He added that the trend is positive news for the metal side of the aerospace industry because single-row planes are mostly made of metal while the two most popular twin-aisle jets are comprised of about 50% components.

Coming down the tarmac is the possibility that another airplane style — the blended wing body — will take to the skies as the industry seeks to significantly reduce carbon emissions. A blended wing airframe is projected to reduce fuel burn and emissions by 50%. “I’m a huge fan,” Aboulafia said. “It’s going to be a long road to get there, but in terms of a potentially transformational new technology, the blended wing body is the best we’ve seen in many, many years.”

Review the print ads from this magazine to continue

This quick advertiser review unlocks the rest of the article and keeps the full-screen reader focused on the ads instead of the page chrome.

MFGAxis Discussion